Carbon Dioxide Removal (CDR) has seen a rapid growth in 2023 amid uncertainties and blows, and set a record high increase in purchases of 437% for the first half this year versus full-year 2022, data according to CDR.fyi.

CDR.fyi is the largest open data platform dedicated to monitor CDR to inform market players and stakeholders with updated data on the industry to help guide investment decisions and scale.

The platform tracks high-permanence CDR purchases and deliveries (100+ years) from public and private data disclosures. Here are the major results in their progress report for the first half of the year.

CDR Purchases Soar, But on the Hands of the Few

Reaching gigatonne-scale of removals each year calls for a very ambitious growth in the industry. Between 40% to 50% annual growth rate by the end of the decade is necessary.

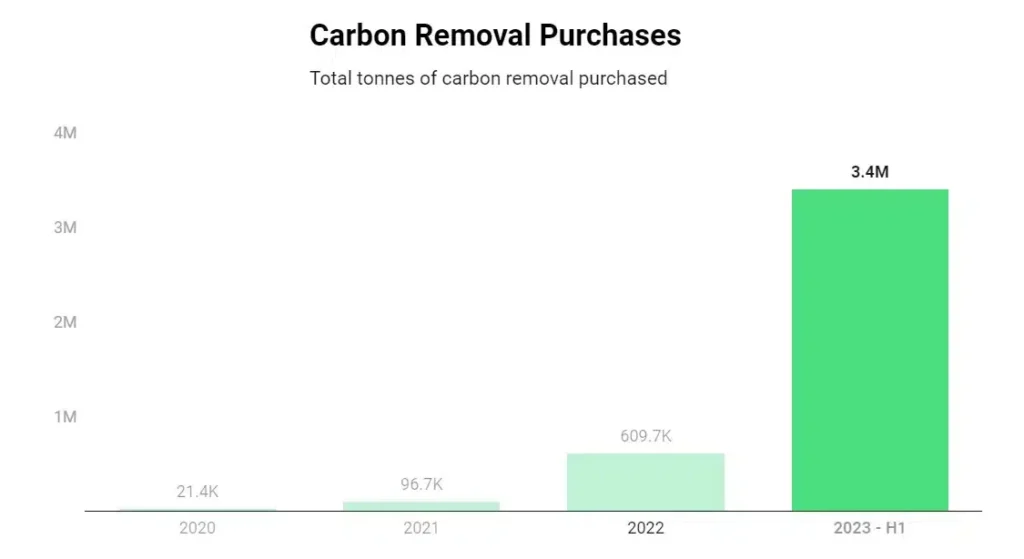

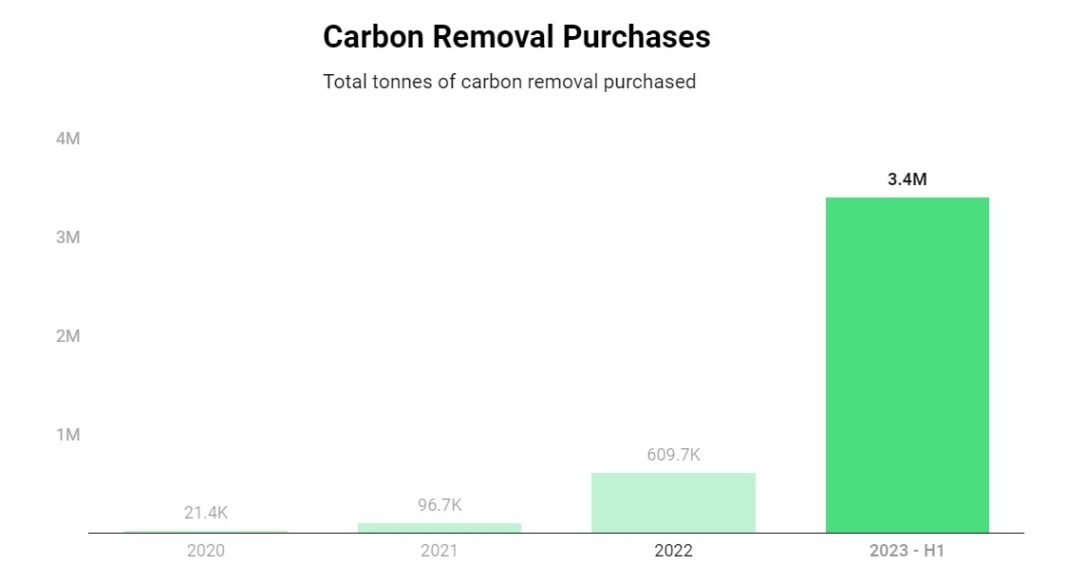

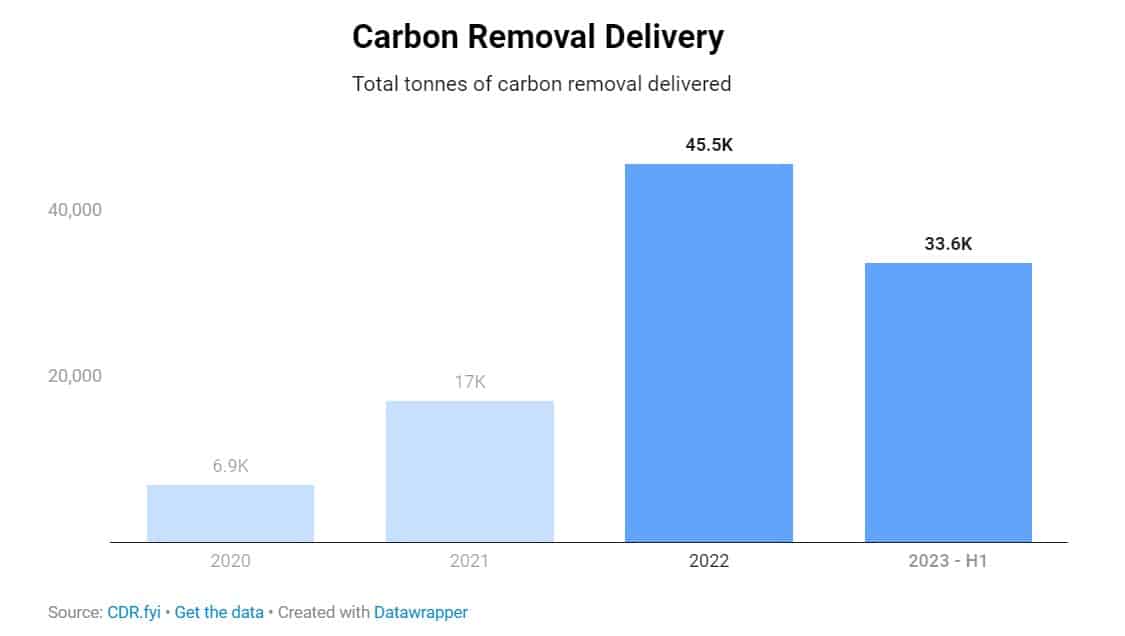

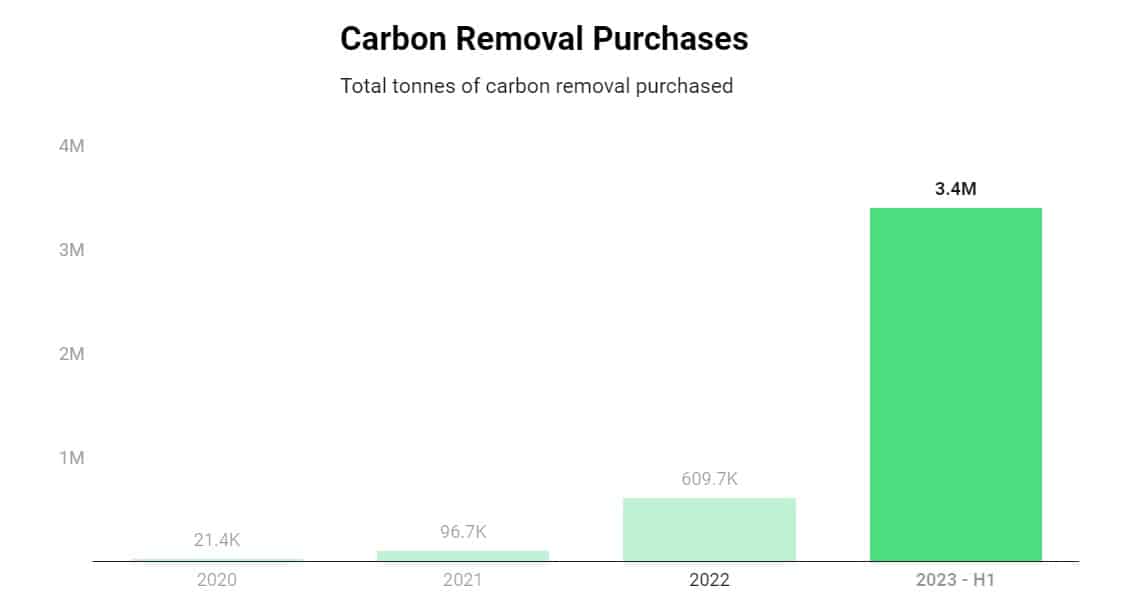

To date, 4.1 million metric tonnes of CDR have been bought, with just 2.6% delivered or ~109k tonnes. But market trends are so promising, showing significant improvements particularly on CDR purchases.

The first half of 2023 has been a defining moment for the CDR market. Purchases surged to about 3.4 million tonnes, showing strong growth of 5.6x versus the full-year 2022.

The whole previous year recorded only around 610 thousand tonnes of CDR purchases.

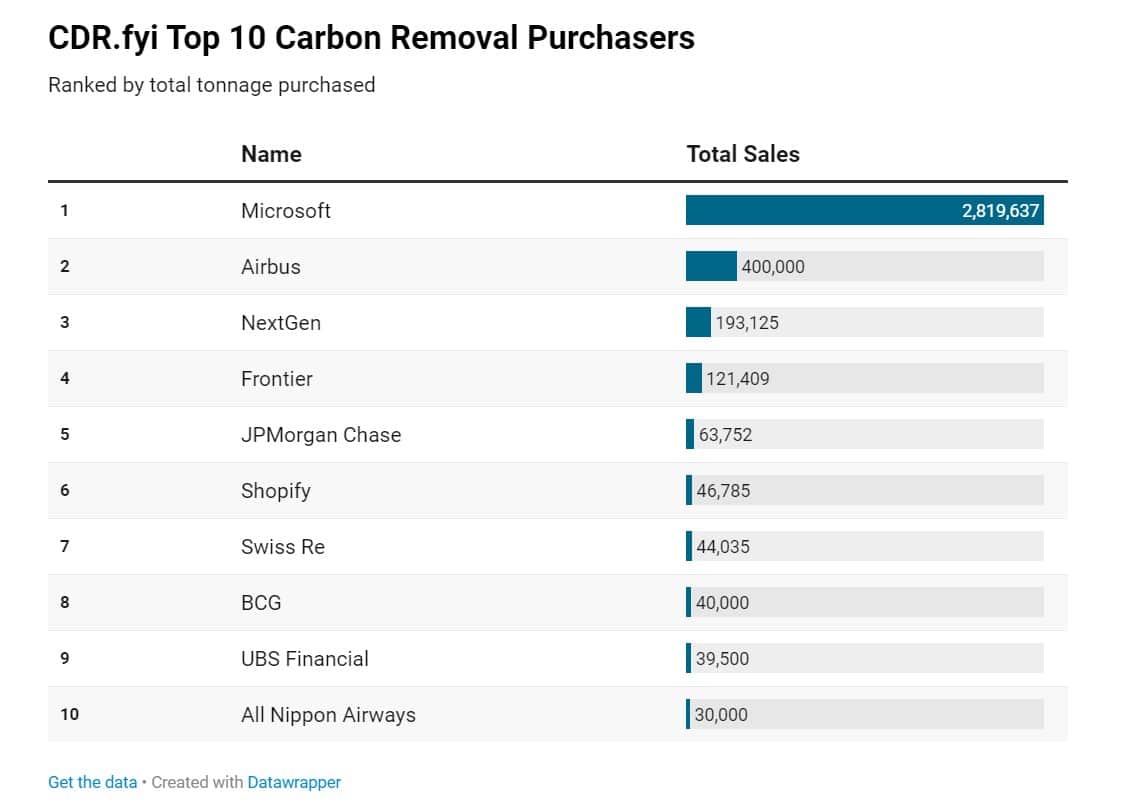

But interestingly, the huge increase is caused by a few major transactions. In particular, the 3 biggest purchase deals are responsible for 95% of the current year’s total purchases. They specifically include the following transactions from large companies:

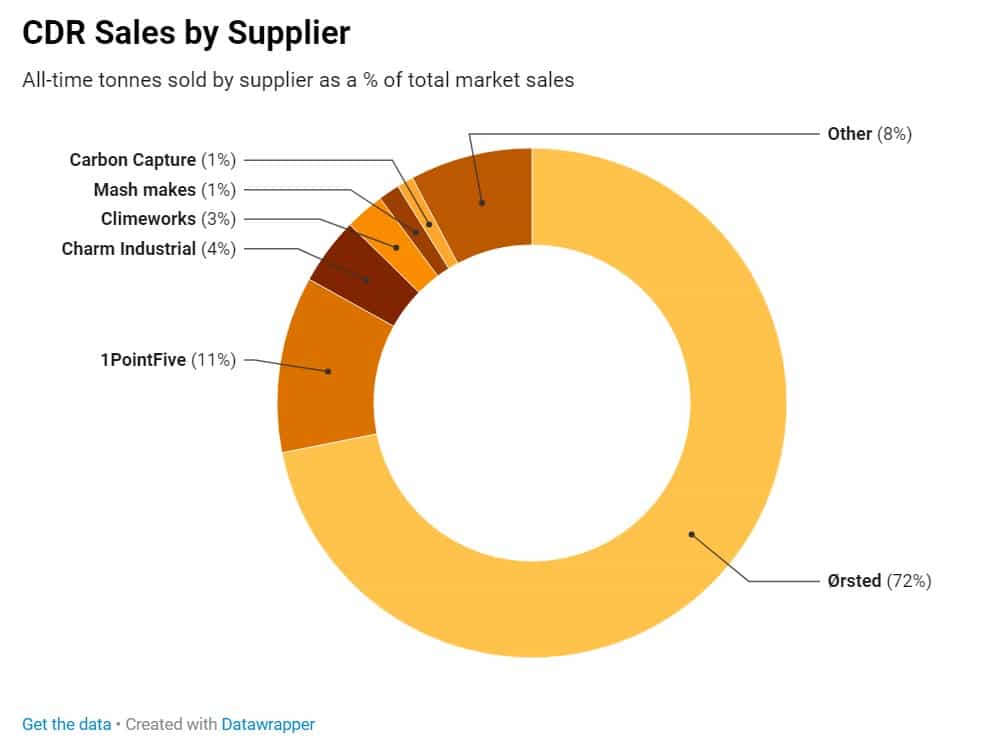

- Ørsted and Microsoft – 2.76 million tonnes of CDR

- NextGen – 193 thousand tonnes

- Frontier and Charm Industrial – 112 thousand tonnes ($53 million)

- JP Morgan – 800 thousand tonnes (with $200 million commitment to buy from Charm, Climeworks, and CO280

Out of those large purchase agreements, delivery of the removals don’t keep up with only over 33 thousand tonnes. Still, it’s higher with a bigger number of suppliers (21) compared to the same period from the past year (19).

The improvement in the length of time from the CDR pre-purchase deal to delivery by more than a year suggests that processes have also improved. This brings more confidence in CDR buyers to make forward purchases.

In fact, corporate CDR buyers are committing to long-term contracts (over 5 years) that align with their net zero targets.

CDR.fyi also reported that the number of CDR buyers in 2023 H1 jumped 14% versus the 2022 H1. And most of them are buying <100 tonnes a year, which is so insignificant compared to the amount of carbon they’re emitting.

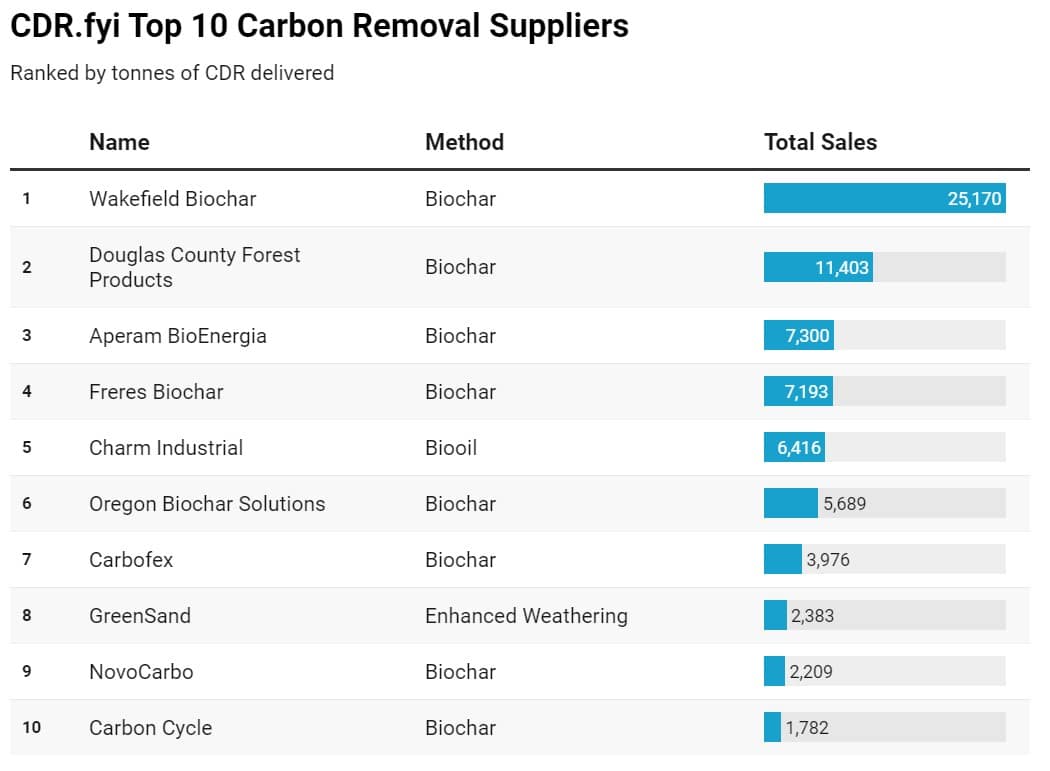

Here are the top 10 in the leaderboards for corporate CDR buyers and suppliers

Diversity in Carbon Removal Methods

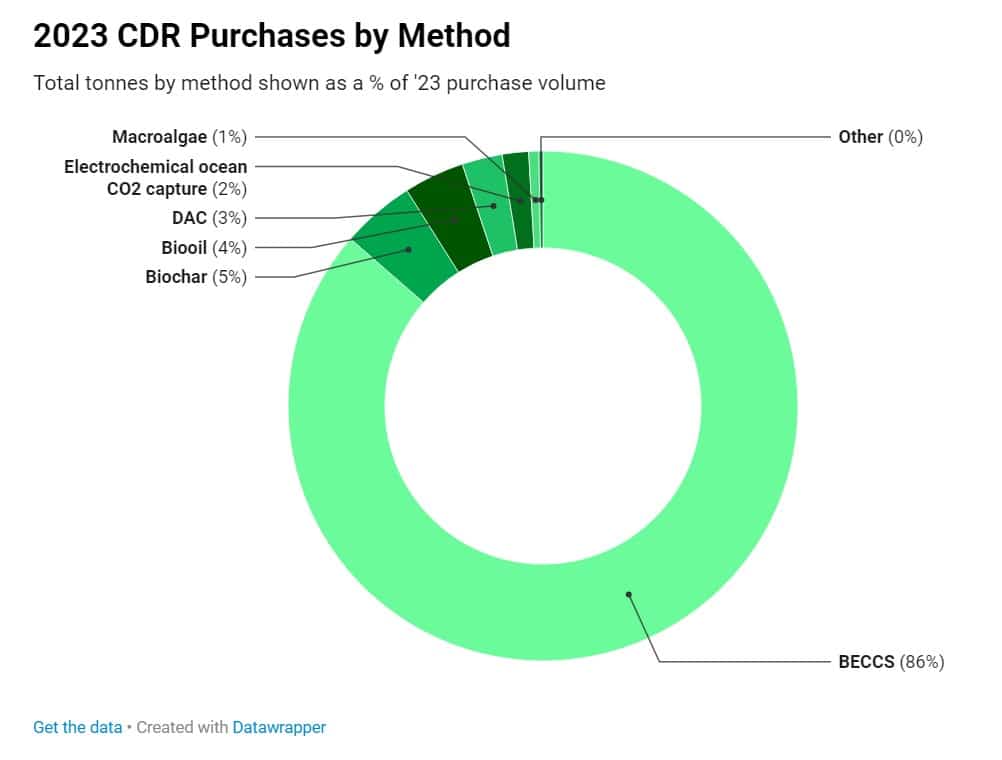

When it comes to CDR methods, CDR.fyi data shows that there are some shifts in distribution trends.

As illustrated in the chart, the bulk of purchases come from BECCS (Bioenergy with Carbon Capture and Storage) – 88%. This is mainly because of the Ørsted and Microsoft CDR deal.

Bio-oil comes next with 4% of the entire volume, Direct Air Capture or DAC represents 3%, while Biochar gets only 2% of CDR purchases. However, it appears interesting to note that CDR from biochar takes up 91% of total deliveries. Bio-oil and enhanced weathering comes second and third, accounting for 6% and 3% of the deliveries respectively.

The diversity in the methods of removing carbon dioxide shows that the CDR market is exploring various ways to mitigate climate change. From ocean-based removal to biomass, these different means also have various levels of potential for scale up. And many of them are in their early-stages that need more investments to reach commercialization.

What the Industry Needs to Scale

The trends are encouraging so far and CDR.fyi further said that by the end of this year, purchases will reach 6 million tonnes. If this happens, it would be a 10x increase from 2022.

However, the fact remains that a lot of major companies are still not in the market. Only a select few are supporting and investing in this emerging carbon credit market.

The report doesn’t include purchases from the governments, which have the capacity to buy CDR at scale. But some progress can be observed in the public sector.

Just recently, the US Department of Energy (DOE) announced its commitment to provide support for CDR suppliers. The agency has been pumping billions of dollars to help scale up the industry. The US government will be the first in the world to provide direct payments to carbon removals suppliers.

As the market continues to deliver high-permanence CDR, we can expect to see more support and investments pouring in. This is critical to enhance the capacity of various methods of carbon removal and bring down the cost of technologies.

Source: carboncredits.com